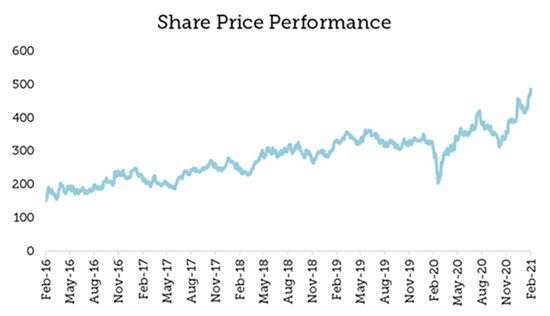

BHP Group - Company snapshot

BHP Group (BHP) is a world-leading resources company - Company snapshot

BHP Group (BHP) is a world-leading resources company - Company snapshot

Commodity Diversification: BHP has a diversified portfolio mix with the contribution to group revenue and EBITDA from the Iron Ore division being 50% and 64%, respectively. Copper contributes 26% to group revenue and 19% to group EBITDA, Coal 15% and 7%, and Petroleum 10% and 10% to group revenue and EBITDA, respectively.

Low-Cost Production: BHP’s high quality asset portfolio stands out among its global peers due to its low-cost position on the cost curve. This enables it to extract competitive margins and better free cash flow (FCF) yields even in market conditions where commodity prices are depressed. It is currently the lowest unit cost producer in Iron Ore, globally.

Balance Sheet Strength: After significant deleveraging, the company has managed to strengthen its balance sheet over the past four financial years and continues to maintain this position. This provides it with better flexibility for future growth and increased cash shareholder returns when compared to its competitors.

Competitive FCF Yields: Its FCF generation is comparable to peers, even with the Petroleum division having been weak in FY20. This provides a potential upside on a recovery in the oil price.

Minimised Risks through Diversification: BHP's diversified portfolio allows it a crucial hedge against commodity price declines in comparison to single-commodity mining companies, which minimises its risks in volatile commodity markets.

Participation in Clean Energy through Copper: BHP is a significant global producer of Copper. Copper helps reduce CO2 emissions and is one of the best renewable sources due to its chemical properties that enable it to reduce the amount of energy needed to produce electricity. BHP’s exposure to copper creates the opportunity for the company to be a contributor to the world’s move into a cleaner energy world, which gives it better future growth prospects than its peers.