How COVID Resistant is Your Fund's Life Stage Solution?

A life stage investment model has two key objectives in mind.

A life stage investment model has two key objectives in mind.

The first quarter of 2020 delivered a rare black swan event in investment markets that most asset managers, investment advisors and retirement fund trustees and members might only experience once in their lifetime. It has been a time during which not only the emotional resilience of Trustees was severely tested but also the effectiveness of the investment strategies and models of their retirement funds. Especially when it involves the interests of those fund members that are close to retirement and who are about to enter the capital consumption part of their lives. Moving member’s fund benefits at the wrong time or in the incorrect manner can be very detrimental to their goal of achieving financial independence at retirement.

Most retirement funds in South Africa have adopted some form of life stage model as part of their default investment strategy. The basic principle behind this model is that the benefits of fund members will be invested in a suitable portfolio that will reflect the investment risk each member can afford on their journey towards retirement. A life stage investment model has two key objectives in mind. The first is to make the retirement fund contributions of every member work as long and as hard as possible in the process of accumulating sufficient capital for retirement. This objective is critical given a structurally weak local economy, a less than desired savings culture, a low preservation ratio when members move between employers and increased longevity. The second objective speaks to the smooth transition from the pre-retirement capital accumulation phase to the capital consumption phase during retirement.

In theory, the life stage model concept sounds like quite a sound and simple solution. However, the significant and rapid drop in market values across a broad range of asset classes during March caused by the COVID-19 pandemic has tested the design and robustness of many life-stage models and their ability to deliver on the above-mentioned objectives.

The first element has less to do with the investment strategy of the fund and relates more to the member communication strategy that supports the life stage model. The most critical moment in any members journey toward retirement is the decision about which type of annuity they will be looking to purchase at retirement. A trigger to communicate with members well before retirement is crucial for ensuring that a member can make an informed decision about the most appropriate investment path to follow as they get closer to retirement. For example, as a result of no or insufficient communication, a member within 2 years of reaching retirement could have been on a Living Annuity path while their actual need was more of a guaranteed Life Annuity nature. This member would run the risk that there is a sharp sell-off in the market with a slow recovery which will leave too little time for their capital value to recover at the point that they need the maximum capital to buy the highest possible income.

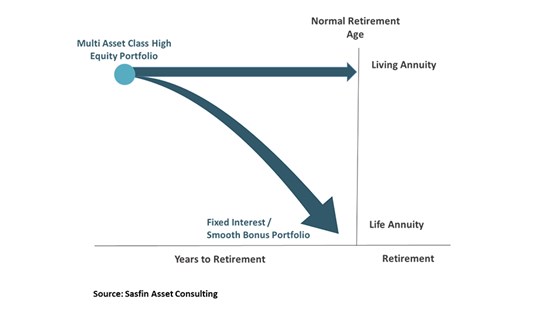

The second key element of an effective life stage model relates to the smoothness of the glide or de-risking path during the last few years before reaching retirement age. This phase involves the gradual reduction of market risk that a member's benefits will be exposed to as they get closer to retirement at which point they will be looking to buy a Life Annuity. If the de-risking phase or glide path is not smooth enough the member's benefits could be moved to a lower risk portfolio at the lowest point of a market correction. The member will effectively lock in capital losses that they cannot recover from even though the market starts to recover again as the lower risk portfolio is not able to capture the market growth. It is important that the glide path of a fund's life stage model allows for smaller, but more regular adjustments to the member's market exposure.

The third element relates to a seamless transition from pre-retirement into retirement for members who are looking to purchase a Living Annuity. The fund's investment strategy should allow a member to remain invested in the same portfolio that they were invested in on the date of retirement when purchasing their Living Annuity. This will avoid any market timing risk and unnecessary costs related to the typical process where the retirement fund benefits are paid out to the member in cash. The member then must arrange for the cash benefit to be re-invested in a different market-related portfolio on a different investment platform. The risk is that the benefits are sold by the fund during a market low. If the cash holding is not invested soon thereafter due to any unforeseen or administrative reasons, then the member might lose out in a V-shaped market recovery scenario. This at a point in time when the member should have stayed invested in the market to avoid missing out on those "top 10 days" in the market.

The final key element relates to the flexibility of the life stage model as it relates to the fund's default annuity strategy. Should the fund have an in fund living annuity as a default annuity the default strategy should cater for the possibility of the member retiring early without putting their capital at risk during a very critical time. Should the member be halfway through the de-risking phase of the life stage model and default annuity strategy should allow the member to effectively continue with the de-risking strategy post-retirement by seamlessly moving the assets into a Living Annuity. Once the de-risking process is complete then the member can buy their preferred guaranteed Life Annuity.

The final years in a fund’s life stage model is a critical part of the journey to retirement as this is a time when the retirement benefits of members are close to reaching their peak. Members have a right to expect that their retirement fund will provide them with the opportunity to maximise the ability to grow their retirement capital while providing the necessary protection of their benefits on their journey towards retirement and during retirement. An effective and well-designed life stage model should allow retirement funds to live up to their member's expectations under any market circumstances. The COVID-19 related market events during March provided a clear invitation to Boards of Trustees and Management Committees to rise to this challenge and once again review their retirement funds’ investment strategies.

Click here to read more about the Sasfin Wealth Umbrella Retirement Fund.