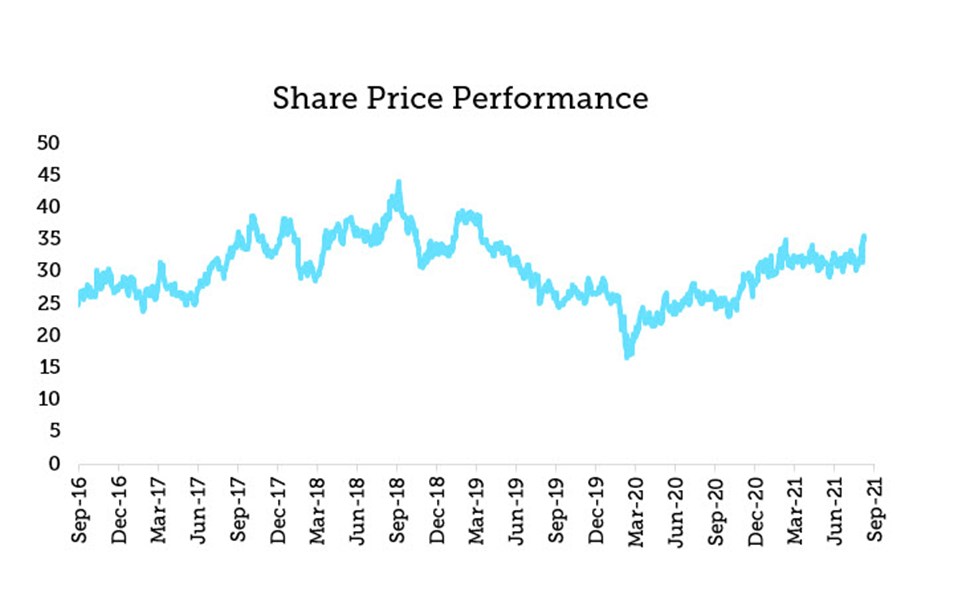

Company Snapshot - South32

In this company snapshot Sasfin’s commodity expert and research analyst, Lwando Ngwane, looks at South32, the key investment drivers and key risks.

In this company snapshot Sasfin’s commodity expert and research analyst, Lwando Ngwane, looks at South32, the key investment drivers and key risks.

Company Overview

Key Investment Drivers

Key Risks