Philip Morris International (PMI) is the largest tobacco company in the world (excluding the Chinese National Tobacco Corporation) engaged in the manufacture and sale of cigarettes, as well as smoke-free products, associated electronic devices and accessories, and other nicotine-containing products in more than 175 markets outside the USA.

The group’s most iconic cigarette brand is Marlboro, the largest global cigarette brand with a market share of approximately 10%, and its key smoke-free brand is IQOS.

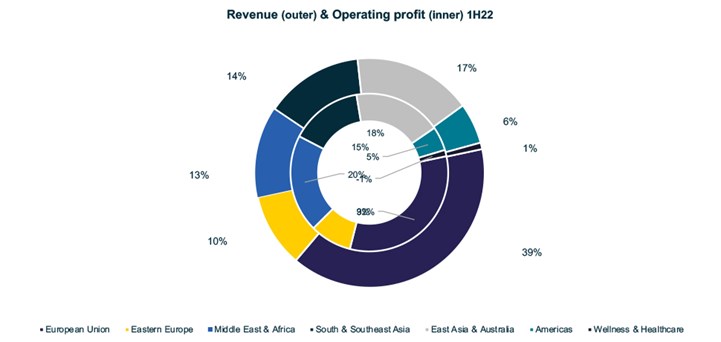

The current product portfolio primarily consists of cigarettes (approximately 70% of sales) and reduced-risk products (30% of sales), including heat-not-burn, vapor and oral nicotine products.

PMI was born when, in 2008 Altria separated Philip Morris USA and its international operations in order to “clear the international tobacco business from the legal and regulatory constraints facing its domestic counterpart, Philip Morris USA”.

PMI and Altria have an agreement whereby PMI sells Altria’s cigarette and e-cigarette brands internationally and Altria will commercialise PMI’s new heated tobacco product, IQOS, in the United States of America (USA) if the Food and Drug Administration (FDA) clears it.

Key Investment Drivers

It is probably worth clarifying that the ‘smoke-free’ policies of many governments seek to discourage the use of harmful combustible tobacco products in favour of less harmful smoke‑free products, and not to ban tobacco use. In fact, evidence shows that lower‑risk New Generation Products (NGPs) lead to accelerated tobacco volume growth. Norway and Sweden, which are close to being ‘smoke‑free’ are recording low single digit nicotine volume growth driven by the high penetration of snus[1] and modern oral tobacco products versus a similar decline in the USA. This suggests that a global transition to NGPs has the potential to at least halt the decades long decline in tobacco volumes, and it favours the business models and valuations of the tobacco companies that are making progress towards smoke-free product portfolios.

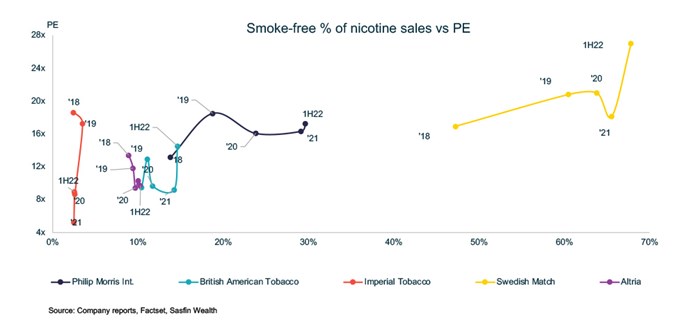

This suggestion is borne out by the above graph, which highlights that: 1) There is a clear positive correlation between the percentage of sales derived from smoke‑free products and price‑earnings (PE) multiple, 2) The absolute level of the PE multiple appears to reflect the pace of progress made toward increasing the smoke‑free revenue exposure, and 3) the generally moderating PE of ‘bond proxy’ consumer staples in 2021/22 within an environment of higher interest rates (see graph overleaf) and higher inflation (impacting pricing power and affordability).

It is no surprise then, that we believe PMI’s proposed acquisition of Swedish Match is a ‘match made in heaven’, albeit ‘complicated’/delayed by hedge fund, Elliot Investment Management’, in an apparent attempt to secure a higher price. The acquisition will position the combined entity as the clear leader in the smoke‑free tobacco space. Swedish Match’s product range spans smoke-free nicotine products such as snus, moist snuff, chewing tobacco and nicotine pouches, with no cigarette exposure. Swedish Match’s combustible exposure comprises of cigars sold in the United States. We estimate that the merger will increase PMI’s smoke-free share of nicotine revenue to over 31%, well on its way to achieve its stated goal of smoke-free products accounting for more than 50% of net revenue by 2025.

Furthermore, PMI stands to benefit from the leveraging off Swedish Match’s distribution infrastructure in the United States (63% of sales in 2021). In our minds, this represents a lower risk, exclusively smoke-free US entry for PMI.

We are equally pleased about PMI’s 2021 acquisitions of Vectura plc, Ferin Pharma and OtiTopic, all leading companies in inhaled, oral and intra‑oral delivery systems. These initiatives add much credibility to PMI’s 2020 stated commitment to build leading scientific capabilities to develop products and services that go Beyond Nicotine.

PMI’s rapidly changing sale composition towards NGPs benefits the group’s profitability in a number of ways, including: i) Smoke‑free products carry a higher sales value than cigarettes and greater profit retention due to lower excise pay-away versus its combustible tobacco products; ii) ongoing progress on achieving around US$2 billion in gross cost savings by 2025; and iii) the sale of margin-dilutive devices is declining as a proportion of revenue (7% in 2020 versus 15% in 2019).

Key Risks

Regulation is probably the primary risk faced by PMI and its peers within the tobacco sector, particularly as it pertains to regulatory authorisation to introduce and commercialise both combustible and NGPs.

The conflict in Ukraine is a set-back to PMI’s medium term NGP targets, as Russia and Ukraine accounted for about 20% of the group’s heated tobacco volumes in FY2021. In aggregate Russia and Ukraine represent marginally more than 10% of PMI's earnings. Rather than run the risk of having its production assets nationalised, as threatened by the Russian government and enforced against French car-maker, Renault, PMI has taken steps to “suspend planned investments and scale down its manufacturing operations in Russia”.

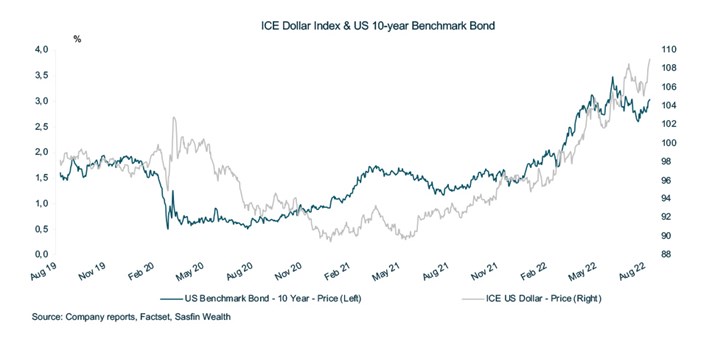

Unfavourable foreign exchange movements are also a key challenge for PMI because it conducts its business primarily in non-US dollar currencies, which are translated into US dollars for the purpose of financial reporting. Hence, during times of a strengthening US dollar, the group’s reported net revenues, operating income and earnings per share will be reduced because the local currency translates into fewer US dollars. Furthermore, during periods of local economic crises, foreign currencies may be devalued significantly against the US dollar, reducing our margins. Actions to recover margins may result in lower volume and a weaker competitive position. Hence, the surge of the US Dollar since 2021, as reflected by the ICE US Dollar Index[1] below, has created strong transaction headwinds.

The US$16 billion offer price for Swedish match will be debt-funded, raising Philip Morris’ net debt to EBITDA (Earnings before Interest, Tax, Depreciation and Amortisation) to approximately 3 times in 2022 from the current level of 1.7 times. The elevated financial risk of this increased debt is amplified within the current environment of aggressively rising interest rates and bond yields and the foreign exchange headwinds on EBITDA. This risk is ameliorated by the fact that at the last financial year (FY2021) Philip Morris’ total debt was ‘primarily fixed rate in nature’ with a weighted average time to maturity of approximately 10 years.