Much like the broader markets, commodities have been exposed to an immense amount of volatility in the first five months of 2022. In the grand scheme of things, the year kicked off with a broad recovery in industrial metal prices following the sharp falls experienced towards the end of last year which were driven by the ‘global energy crunch’. Metal price moves have been torn between conflicting drivers on the supply and demand sides. COVID-19 has continued to weigh on commodities. Additionally, the Russia/Ukraine war combined with supply constraints and concerns over China have all added to the volatility in the commodities markets.

The S&P Goldman Sachs Commodity Index (GSCI) which tracks the agriculture, energy, industrial metals, livestock and precious metals sectors ended the month of January 11% up. In February, it added a further 8%. Between the start of the year and March 31st, the index was up 40%.

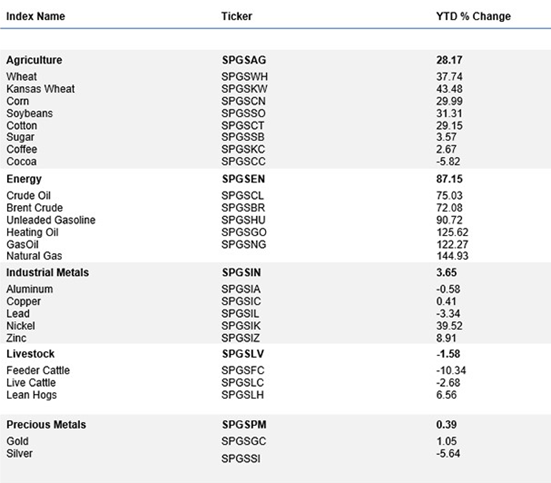

Year-to-date (YTD), the GSCI is up 54.4%, with almost all the positive performance being attributable to the energy sector which Is up 87%, followed by agriculture which is up 28%. The worst performing sector has been livestock, down 2% YTD. Precious metals are flat, while industrial metals are up 4% YTD. Chinese lockdowns, slowing GDP growth and the devaluation of the yuan, combined with the EU decision to exclude base metals such as aluminum and copper from sanctions on Russia continue to weigh on most metal prices as we move towards the end of the first half of 2022. Below is a performance summary of the sector.